Many may be unaware

that General Ledger (GL) accounting does not work for

insurance premium and return premium transactions. As evidence

of this inadequacy, one may cite current agency management

systems inability to generate a Balance Sheet of premium

trust funds. Without a Balance Sheet, insurance trust account

financial solvency cannot be reported and therefore controlled

as required by law.

Another element of

evidence is GL accountings failure to create accounting

records of insurance policy premium transaction, the true

legally binding sale document of an insurance

policy.

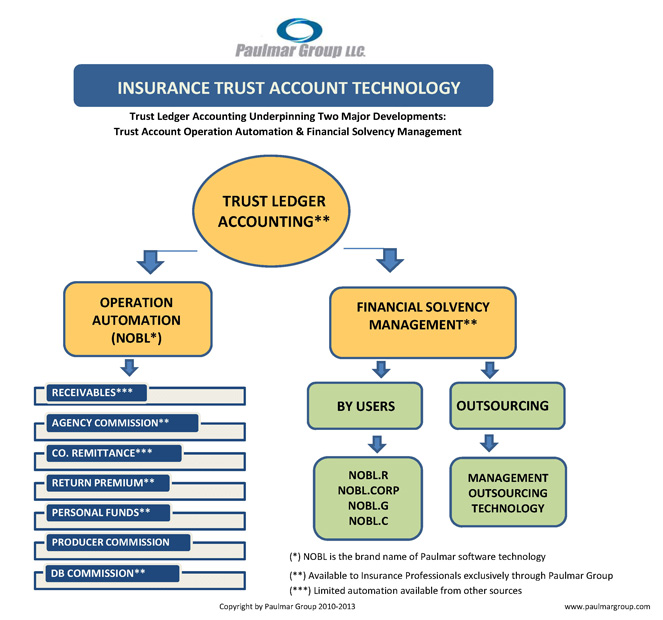

Replacing

GL Accounting

Trust Ledger (TL)

Accounting was developed to replace GL accounting in the

P&C insurance brokerage industry. Unlike GL accounting, TL

accounting can generate trust account Balance Sheets as well

as Premium Float Statements (similar to Profit & Loss

Statements). The latter are critical in determining trust

account cash balance beneficiaries.

Two Major

Developments

Trust Ledger

Accounting made possible two major developments: (1)

automation of the trust account daily operations and

accounting transactions and (2) financial solvency management.

Trust account operation is in many ways different than a

general business operation; it can also be much more complex.

It includes:

1.

Premium

Receivables

2.

Agency Commission

3.

Company

Remittance

4.

Return Premiums

5.

Personal

Funds

6.

Producer

Commission

7.

Direct Bill (DB)

Commission

Financial Solvency

Management includes a reporting system that enables users to

monitor and control premium funds financial solvency on a

daily basis.

In-House or

Outsourcing

Financial Solvency

Management may be carried out in-house or outsourced. The

first option enables users to outsource software applications

such as:

·

NOBL.R for use by

P&C insurance retailers

·

NOBL.Corp for use

by corporations with multi-producer agencies or

clusters

·

NOBL.G for use by

P&C general managing agencies (currently under

development)

·

NOBL.C for use by

insurance carriers (currently under

development)

The second option

is available to those users interested in outsourcing the

trust account management (in the same way they outsource the

payroll). Users provide source documents; an outsourcing

partner will manage premium and return premium funds from the

time they are transacted until they are disbursed to legal

owners.

Agencies will

receive their commission income while net premiums are

remitted to carriers and return premiums refunded to insureds.

Management

Outsourcing Technology was developed to render the cost of

outsourcing economically feasible and a service deployment

with no disruption to the agencys ongoing

business.